Usage metering is getting absorbed

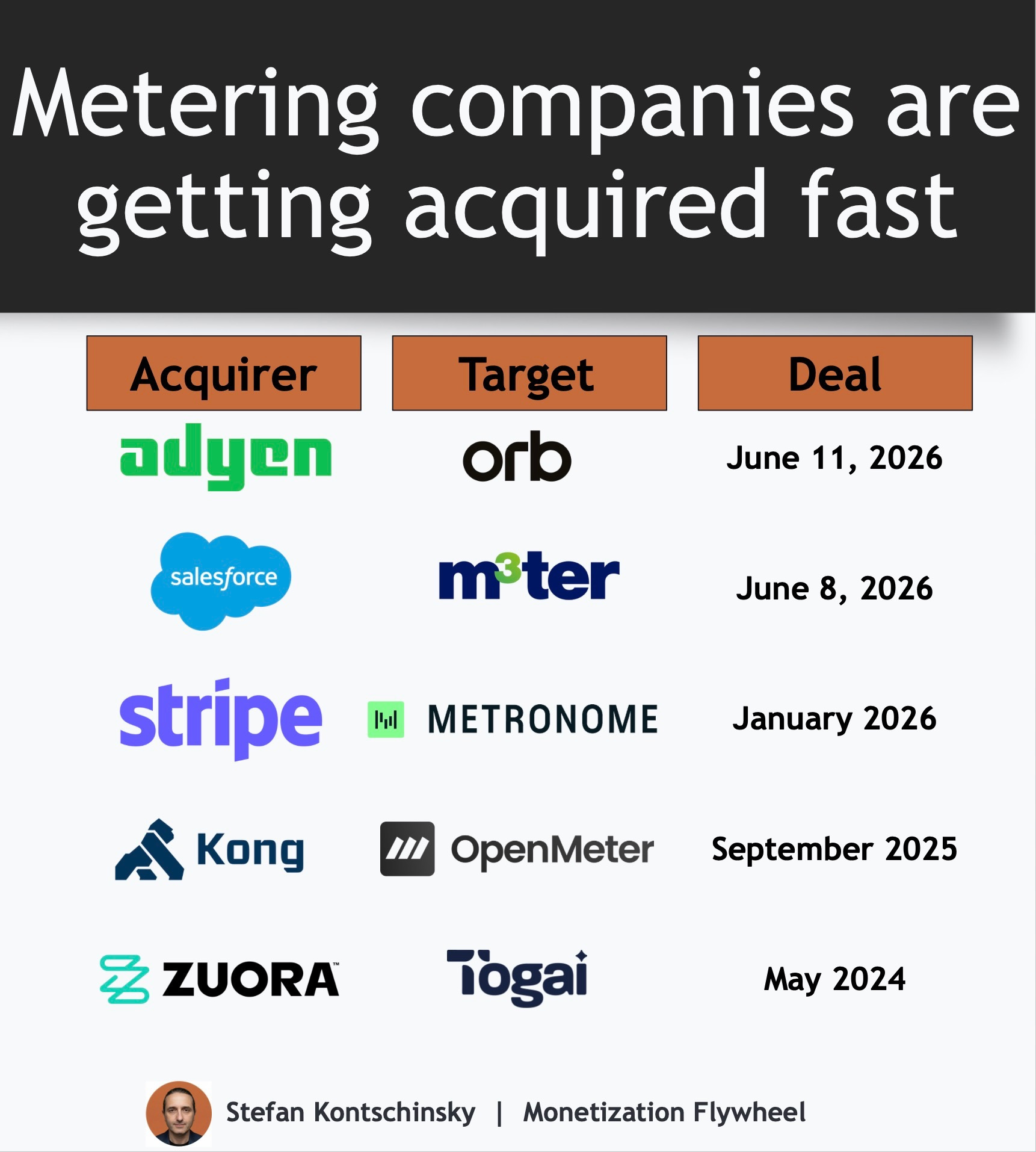

Salesforce acquired m3ter on June 8th. Adyen acquired Orb on June 11th.

Two usage metering acquisitions in four days. Five in 25 months.

AI usage pricing requires metering usage at scale, and billing accurately based on that usage. That created a new infrastructure category: usage-native metering and rating platforms such as Metronome, m3ter, Orb, OpenMeter, and Togai.

Zuora, Kong, Stripe, Salesforce, and Adyen have all moved to acquire that layer that turns product consumption into billable revenue. The meter is getting absorbed into the systems that already own the revenue workflow: payments, CRM, API infrastructure and subscription billing. The pace has accelerated.

Why metering tools exist

Billing AI usage has two hard parts: metering and rating.

Metering is observing and recording raw usage events. Events are API calls, tokens processed, GB transferred or GPU-second consumed. That sounds simple until you are ingesting millions of events per minute in real time across thousands of customers, with full auditability for every one.

Rating takes those counted events and applies your pricing logic to them, converting usage into numbers, e.g.

Tiered limits that reset monthly

Overage charges once included balances are drawn down

Minimum commitments that floor the invoice

Volume discounts that kick in at thresholds

Custom contract terms that override standard pricing

The two functions are separated by design. You can meter perfectly and rate wrong. You can have correct pricing logic but incorrectly meter events upstream. B2B contracts make this specifically hard for three reasons:

The scale problem: AI companies’ token consumption has orders of magnitude more events than what SaaS billing systems were designed to handle. Think of metering millions of events per minute vs. thousands of seats per month.

The flexibility problem: Usage-based pricing models iterate constantly. Rob Litterst from PricingSaaS reported on average more than 3 pricing changes per company in 2025, with fast-growing companies making multiple pricing changes per month. Each change needs to flow through the rating engine without an engineering sprint.

The auditability problem: Revenue recognition requires a complete event ledger. Every metered charge needs a traceable lineage from raw event to billable line item. If you cannot defend a charge when a customer disputes an invoice, you will lose trust.

A small set of purpose-built companies emerged to solve this. They became the infrastructure layer for billing AI usage. Now larger platforms started acquiring that capability rather than building it.

The M&A wave

Five acquisitions, five different acquirers, the same underlying logic: a platform that already owns part of the revenue workflow acquires the metering and rating layer it was missing.

Adyen + Orb (announced June 11, 2026)

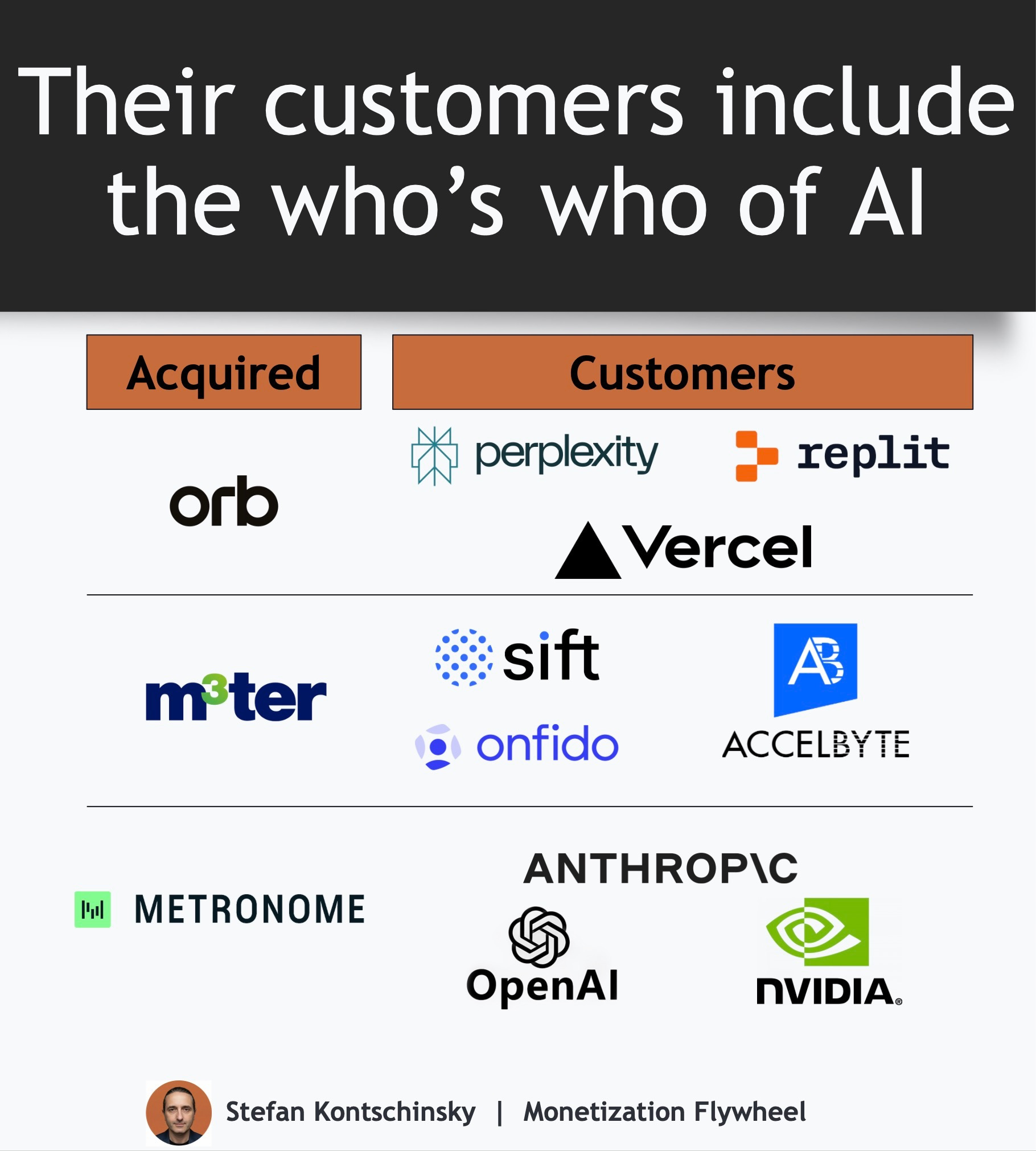

Adyen already serves customers like Uber and Spotify. Orb’s customers include Perplexity, Replit and Vercel. Orb lets engineering teams define billing metrics directly with SQL queries, simulate pricing changes against historical usage data before deploying in production, and report on usage in real-time. Orb CEO Alvaro Morales on the rationale of bringing both together:

“Standalone billing systems are fundamentally limited because they operate blind to transaction execution … By joining forces with Adyen, we can connect this ingestion layer directly to real-time financial health signals, closing the loop between billing logic and payment success.”

Prior to its acquisition by Adyen, Orb had raised $44M, including $25M from its Series B in September 2024.

Salesforce + m3ter (announced June 8, 2026)

Salesforce already owns the CRM, CPQ, and increasingly the agentic workflow layer. Without a metering engine, they couldn’t close the loop on consumption-based AI monetization. m3ter gives them enterprise-grade rating inside Revenue Cloud.

Salesforce framed it directly: acquiring m3ter to

“bring high-volume mediation, metering and rating capabilities natively to Agentforce Revenue Management, enabling enterprises to launch, track, scale, and bill with the flexible usage and outcome-based pricing models needed for the AI era.”

m3ter had raised $31.5M before its acquisition. Latka estimated the deal cost Salesforce around $140M.

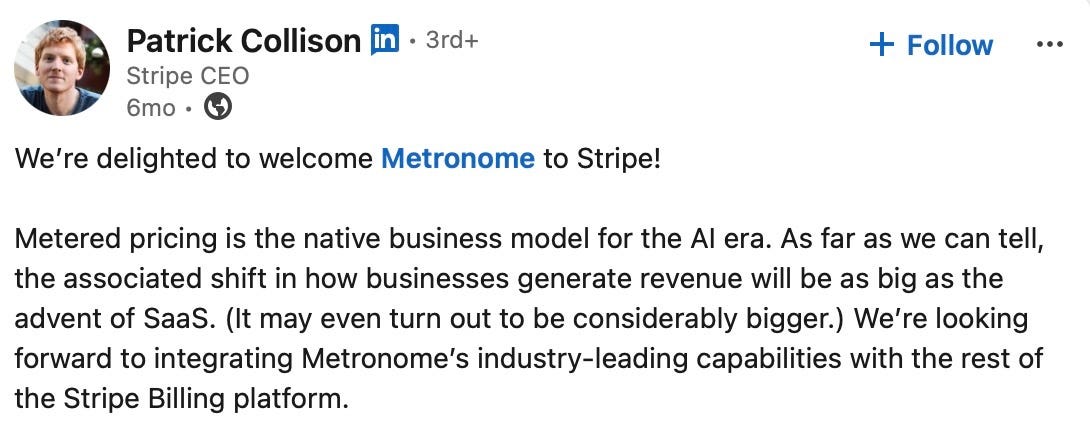

Stripe + Metronome (completed January 2026, reported ~$1B)

Metronome’s customer list reads like an AI infrastructure directory: OpenAI, Anthropic, Confluent, and Nvidia. Stripe CEO Patrick Collison was plain:

”Metered pricing is the native business model for the AI era.”

Metronome had raised $128M, including a $50M Series C just months before the deal. Stripe reportedly paid around $1B, ~2.1x Metronome’s last $470M valuation, per Sacra.

Kong + OpenMeter (acquired September 2025)

Kong is the API gateway and already sits in the traffic path for API calls. Adding OpenMeter means Kong can now translate that traffic directly into billable events. The API gateway becomes part of the monetization system.

“OpenMeter’s capabilities will be integrated into Kong Konnect, enabling usage-based pricing, entitlements, and invoicing for APIs, events, and AI workloads.”

OpenMeter had raised $3M prior to the acquisition.

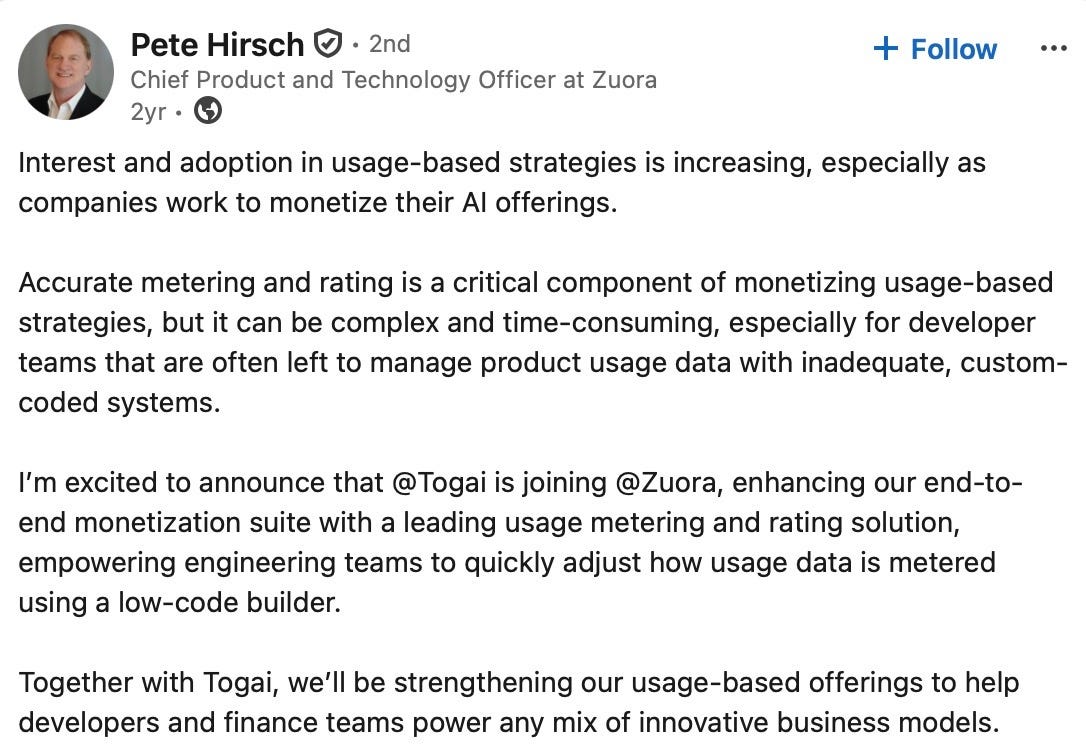

Zuora + Togai (acquired in May 2024)

Zuora has owned subscription billing for years but was architecturally weak on usage.

“Togai’s low-code builder and developer-friendly interface to quickly configure metering and rating of raw events” filled the gap without Zuora having to rebuild its core engine.

Zuora acquired Togai for $24.3M. Togai had raised $3.1M prior to its acquisition.

The pattern across all five:

Five different players, all move into usage metering and rating:

Orb → Adyen = Payments + Billing + AI consumption metering

m3ter → Salesforce = Enteprise CRM + AI consumption metering/rating

Metronome → Stripe = Payments + Billing + AI consumption metering

OpenMeter → Kong = API gateway + API usage rating

Togai → Zuora = Subscription monetization suite + usage rating

Who’s left standing

Not everyone got acquired. Two notable independent players are still building as standalone companies, and their positioning reveals what they’re betting on.

Sequence goes wider than pure metering. It positions itself as a CPQ + billing + usage metering + revenue recognition + receivables automation platform. Their customers include Cognition, Legora and 11x. Their bet is fast-scaling AI companies need one platform for the entire workflow from contract signature to accurate billing. Sequence raised $38M from investors like 645 Ventures and a16z, including $20M from a Series A in December 2025.

Lago is the open-source bet. Customers include Groq and Mistral.ai. It allows AI labs to self-host and control their billing infrastructure. Lago’s differentiation is deployment flexibility: fully managed cloud or on-premises, with full access to the underlying data. For companies with data residency requirements or platform independence as a strategic priority, Lago is the natural alternative to the lock-in that comes with being inside Stripe’s or Adyen’s billing stack. Lago raised $22M from investors like FirstMark, SignalFire and Y Combinator. Its Series A valued it at reportedly $100M.

What this means for pricing strategy

For Pricing teams, metering is becoming a platform capability. Instead of having to buy a separate metering tool, Pricing teams can leverage their existing CRM / Billing / API gateway. That might make it a little easier to secure a budget for metering.

For founders building on AI, billing infrastructure is now a platform alignment choice. The vendor that owns your metering has full visibility into your unit economics: consumption patterns, pricing model structure, which customers have custom contract terms, where you draw overage thresholds. The vendor that owns your metering owns your pricing intelligence. That leverage matters the next time you’re renewing with them.

For the remaining standalone players, Lago and Sequence, a strategic acquisition looks like the most plausible path. The obvious buyers are platforms that already own parts of the revenue workflow but have not yet acquired a usage-native metering and rating specialist: Microsoft, ServiceNow, HubSpot, or larger billing incumbents like Chargebee, BillingPlatform, and keylight. Those billing incumbents already support subscription, usage-based, and hybrid models, but as AI monetization keeps pushing toward event-native metering, real-time rating, and constant pricing iteration, they may still decide that owning deeper metering infrastructure matters.

The window for those acquisitions is closing. Once the category fully consolidates, founders building AI products will have to commit to a wider platform when choosing their metering and rating engine.

Great article 👏