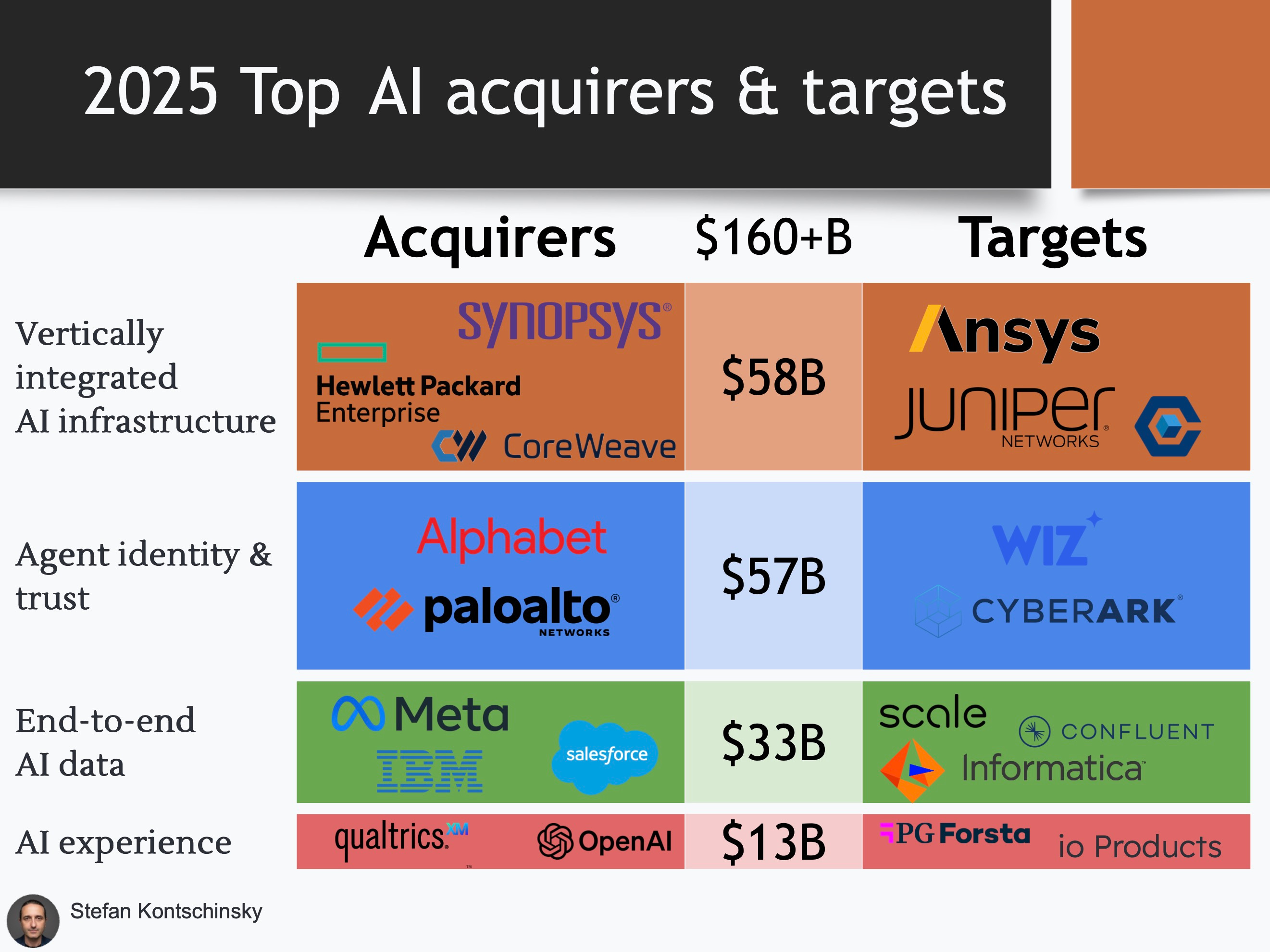

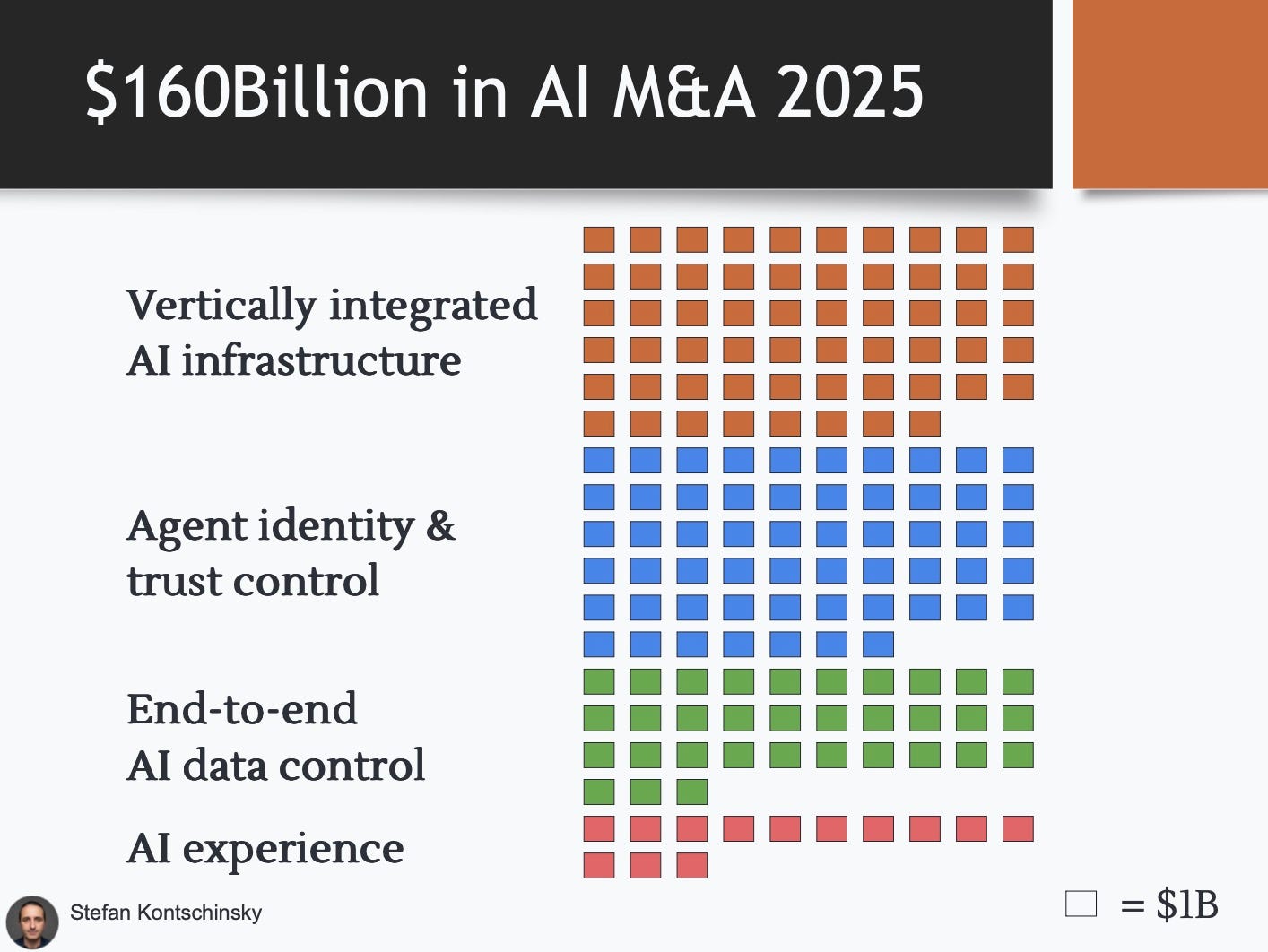

$160+B of AI M&A in 2025.

The 10 largest deals locked in architecture and control across four layers.

While headlines focused on frontier model funding rounds, M&A committed buyers to how AI systems will actually be built, governed, and operated, with decisions that are hard to unwind.

Funding builds options. It keeps architectures flexible and narratives open.

M&A hardens decisions, collapses layers, and locks in the control layers where leverage compounds, switching costs rise, and architectural choices become durable.

Those control layers are infrastructure, identity, data, and experience.

1) Vertically integrated AI infrastructure

(Simulation → silicon → networking → compute)

Deals:

Synopsys acquired Ansys (AI simulation and chip design) for $35B in July 2025.

Hewlett Packard Enterprise acquired Juniper Networks (AI-native data center networking) for $14B in July 2025.

CoreWeave acquired Core Scientific (High-density AI compute) for $7B in July 2025.

What is converging:

AI workloads are forcing tight coupling across layers that were historically modular. Simulation, chip design, networking, power, and compute are collapsing into a unified layer. Scale is becoming the competitive moat.

Why it matters:

This signals the end of best-of-breed infrastructure for frontier AI. The winners own the entire infrastructure stack, from silicon to compute.

2) Agent identity & trust

(Human identities → agent identities)

Deals:

Alphabet acquired Wiz (Cloud and AI-native security posture management) for $32B in July 2025.

Palo Alto Networks acquired CyberArk (Identity for machine and agent access) for $25B in July 2025.

What is converging:

Identity security, cloud posture, and runtime protection are merging into agent-aware trust layers. The perimeter is no longer users or workloads. It is autonomous AI agents acting independently.

Why it matters:

This is the creation of control infrastructure for non-human identities as agents inside enterprises require new controls.

3) End-to-end data

(Raw data → labeled data → real-time inference)

Deals:

Meta Platforms invested $14B in Scale AI (Data labeling for AI applications) in April 2025.

IBM acquired Confluent (Real-time data streaming for AI systems) for $10B in May 2025.

Salesforce acquired Informatica (Enterprise AI data governance) for $8B in June 2025.

What is converging:

Data ingestion, labeling, governance, and activation are collapsing into AI-ready data layer. The distinction between operational data and big data is disappearing.

Why it matters:

Owning the data lifecycle becomes more valuable than owning models. Models churn. Data moats compound.

4) AI experience and interactions

(Dashboards → continuous, ambient AI)

Deals:

Qualtrics acquired Press Ganey Forsta (AI experience measurement) for $8B in June 2025.

OpenAI acquired io Products (Always-on AI device) for $6B in September 2025.

What is converging:

Experience measurement, feedback loops, and interaction surfaces are becoming continuous and embedded. Hardware, software, and inference are merging into always-on experience systems.

Why it matters:

The experience is shifting from UX to continuous presence. AI is no longer something you open as an app. It is always on and with you.

5) The July 2025 deal cluster & the meta-convergence

More than half of the top 10 AI deals in 2025 closed in July alone. I had posted about the spree at that time here. The July cluster was structural, because by mid-year three things had changed:

Cost for compute and inference were better understood. Stanford’s 2025 AI Index Report from April 2025 found hardware costs declined ~30% annually, and energy efficiency improved by ~40% each year.

Confidence in enterprise demand for AI showed and Nvidia’s stock price increased 70+% from low of $94 in April 2025 into new all time highs of $160+ for the first time.

Buyers had H1 performance visibility and board-level approval to commit capital at scale. AI wasn’t experimental any longer.

That made future cost for real use cases predictably cheaper, increased confidence that growing demand is real, and allowed large transactions to act swiftly.

Closing Thought

The 2025 M&A wave showed where power actually compounds. Point solutions get absorbed. Control layers become the long-term profit centers.

If you are building or investing in AI, the critical question is which layer you own, and how durable that position is as the stack continues to consolidate.