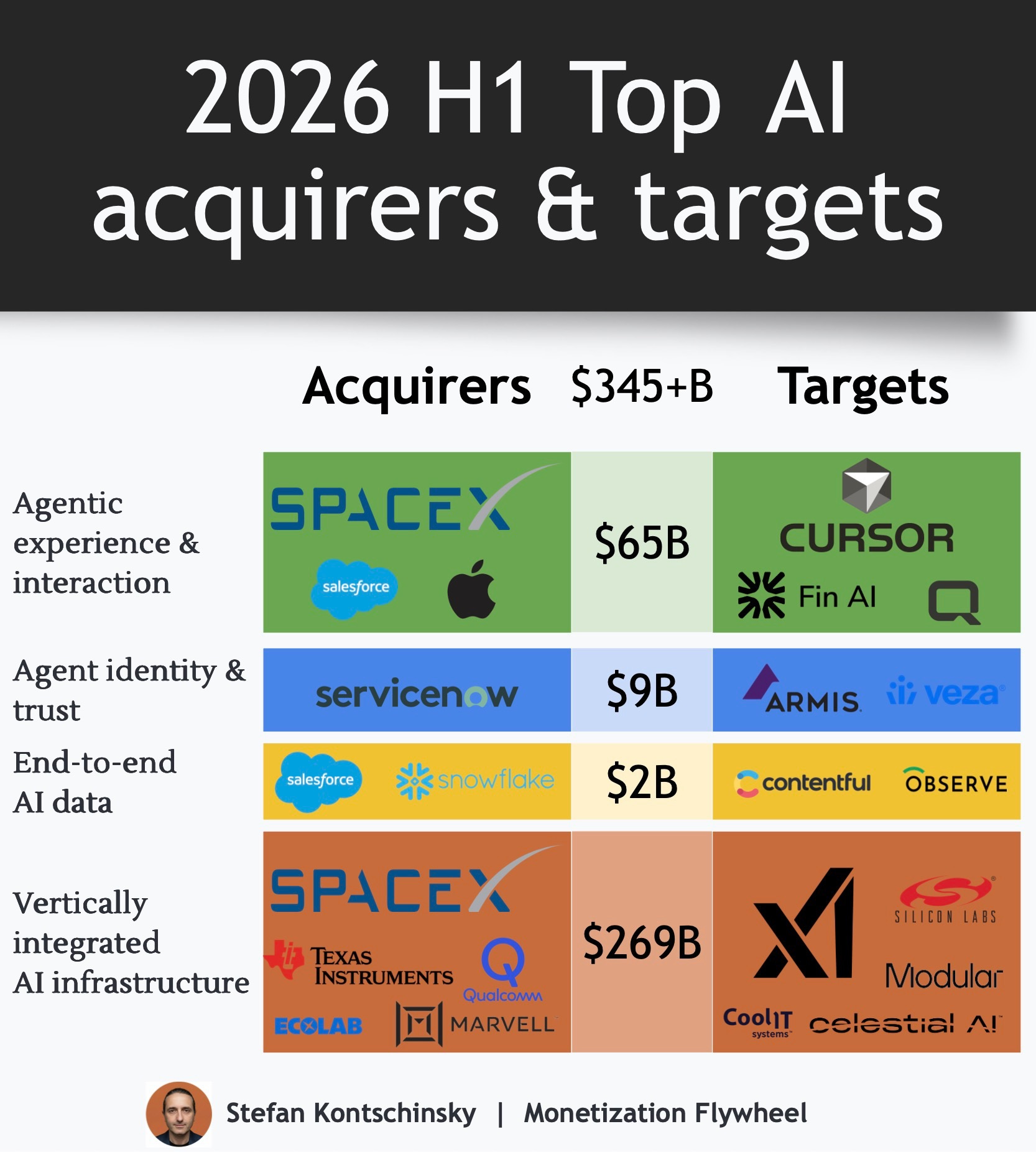

$345B+ of AI M&A in H1 2026

SpaceX dominated ~90% and now sells AI infrastructure to Claude and OpenAI

Last year, the AI consolidation started in each of four layers: infrastructure, identity, data, and experience. Different buyers consolidated in each one. The labs themselves stayed independent and kept raising. Read my post on it here.

Halfway through 2026, the big acquirers started reaching across several layers at once. This locks in the control points where leverage compounds, switching costs rise, and architectural choices become durable.

The main difference in 2026 so far is also in concentration: SpaceX moved across the layers fast, and at larger scale, than anyone else. Here are the 10 biggest deals:

1) Vertically integrated AI infrastructure

(Silicon → power & cooling → interconnect → compute)

Deals:

SpaceX acquired xAI (the Colossus supercomputers, Grok, X) for $250B in February 2026.

Texas Instruments acquired Silicon Labs (connectivity and edge silicon for AI devices and data centers) for $7.5B in February 2026.

Ecolab acquired CoolIT Systems (direct liquid cooling for AI data centers) for $4.75B in March 2026.

Qualcomm acquired Modular (hardware-agnostic AI inference and compute stack) for ~$3.9B in June 2026.

Marvell acquired Celestial AI (silicon photonics and optical interconnect) for $3.25B, up to $5.5B with earnouts (announced Dec 2025, closed Feb 2026).

What is converging: Last year this layer collapsed simulation, silicon, networking, and compute into one stack. In 2026 it extended in two directions. Down into power and thermal, and up into the supercomputer itself.

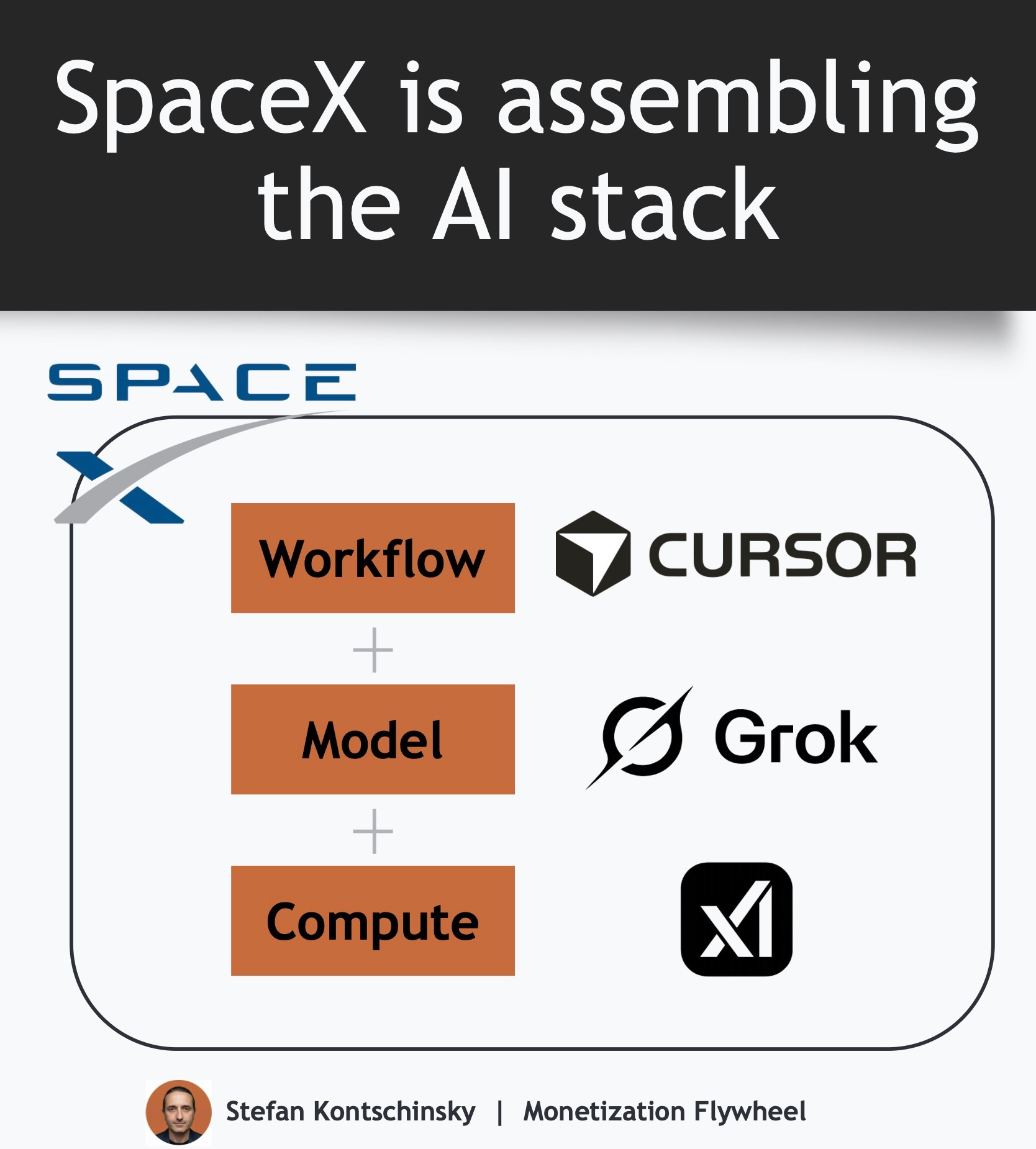

xAI is the apex of that. It covered three layers at once: It captured the compute (Colossus’ 555,000-GPU cluster drawing two gigawatts, the gas turbines and substations feeding it & the planned orbital data centers), the model (Grok), and the distribution and identity surface (X).

And SpaceX now even rents xAI compute out to other AI providers. Anthropic took all of Colossus 1, more than 220,000 GPUs and over 300 megawatts, to serve Claude. Google took capacity in Colossus 2 through 2029 for $920M per month!

Why it matters: The AI infrastructure moat is now physical and full-stack. Power, cooling, photonic interconnect, and the supercomputer itself. Owning an AI data center is becoming as defensible as making the AI chips.

The year’s biggest compute commitments that were not acquisitions point the same way. Meta and OpenAI both signed commitments with CoreWeave for $21B and $22.4B respectively. Those were capacity contracts though, not transfers of ownership, so I left them out.

2) Agentic experience & interaction

(Apps → agents → ambient AI)

Deals:

SpaceX acquired Cursor / Anysphere (AI coding) for $60B in June 2026. SpaceX used its newly public stock to fold Cursor in days after the IPO.

Salesforce acquired Fin / Intercom (autonomous customer-service agents) for $3.6B in June 2026.

Apple acquired Q.ai (silent-speech and on-device audio AI) for ~$1.6B in January 2026.

What is converging: The interaction surface is splitting two ways. Toward agents that resolve work end-to-end (Fin in service, Cursor in code). And toward ambient, on-device sensing that removes the interface (Q.ai reads mouthed and whispered words from facial micro-movements).

Why it matters: SpaceX bought its way into enterprise workflows by buying the coding AI. Apple bought its way back toward frontier AI through audio and imaging in its second-largest acquisition ever.

3) Agent identity & trust

(Human identities → agent identities)

Deals:

ServiceNow acquired Armis (AI-powered cyber asset and exposure management) for $7.75B (announced December 2025, closed April 2026).

ServiceNow acquired Veza (AI-native identity for human, machine, and agent access) for ~$1B weeks earlier.

What is converging: Asset visibility, exposure management, and permission mapping are merging into a single agent-aware trust layer. ServiceNow stitched what an enterprise has (Armis) to what every identity can do (Veza). It built the combination explicitly to govern autonomous agents.

Why it matters: As agents take real actions inside enterprises, the control point is shifting from the user login to the permission graph for non-human identities. Similar to the Wiz/CyberArk logic of 2025, ServiceNow in 2026 has bought its identity stack.

4) End-to-end data & agent context

(Raw data → telemetry → grounded agent context)

Deals:

Salesforce acquired Contentful (composable content layer for AI agents) for ~$1-1.5B in June 2026.

Snowflake acquired Observe (AI-powered observability and telemetry) for ~$1B in January 2026.

What is converging: Data, content, and telemetry are merging into the context layer that grounds what agents do. The platform has to feed agents the right content to act on and watch the actions they take.

Why it matters: “Models churn. Data moat compounds.” That was my 2025 data-moat thesis, and it extended in 2026 to governance of the live content and telemetry that agents read and write. Owning the context is owning the agent’s version of reality.

5) The June cluster & the meta-convergence

In the first half of 2025, inference became better understood and confidence in enterprise demand for AI rose. That fueled a consolidation of point solutions across the 4 layers of the AI stack in the second half of the year (I wrote about it here).

And just as more than half of 2025’s top deals landed in a single July spree, 2026’s biggest deals clustered around one event. SpaceX went public on June 12. Days later it used its freshly liquid stock to buy Cursor for $60B. Salesforce announced Fin and Contentful in the same stretch.

Four things changed the shape of the year:

SpaceX dominated. xAI and Cursor together were $310B, that is ~90% of the total 2026 H1 M&A. That concentration is extreme. Strip out the Musk empire and the top 10 are ~$35B and more evenly spread across every layer. Salesforce was the other major player that consolidated across two layers (Contentful data + Fin experience). SpaceX wrote the headlines and reached across infrastructure (xAI Colossus), model data (Grok), and experience (X) with the xAI deal, then added Cursor too.

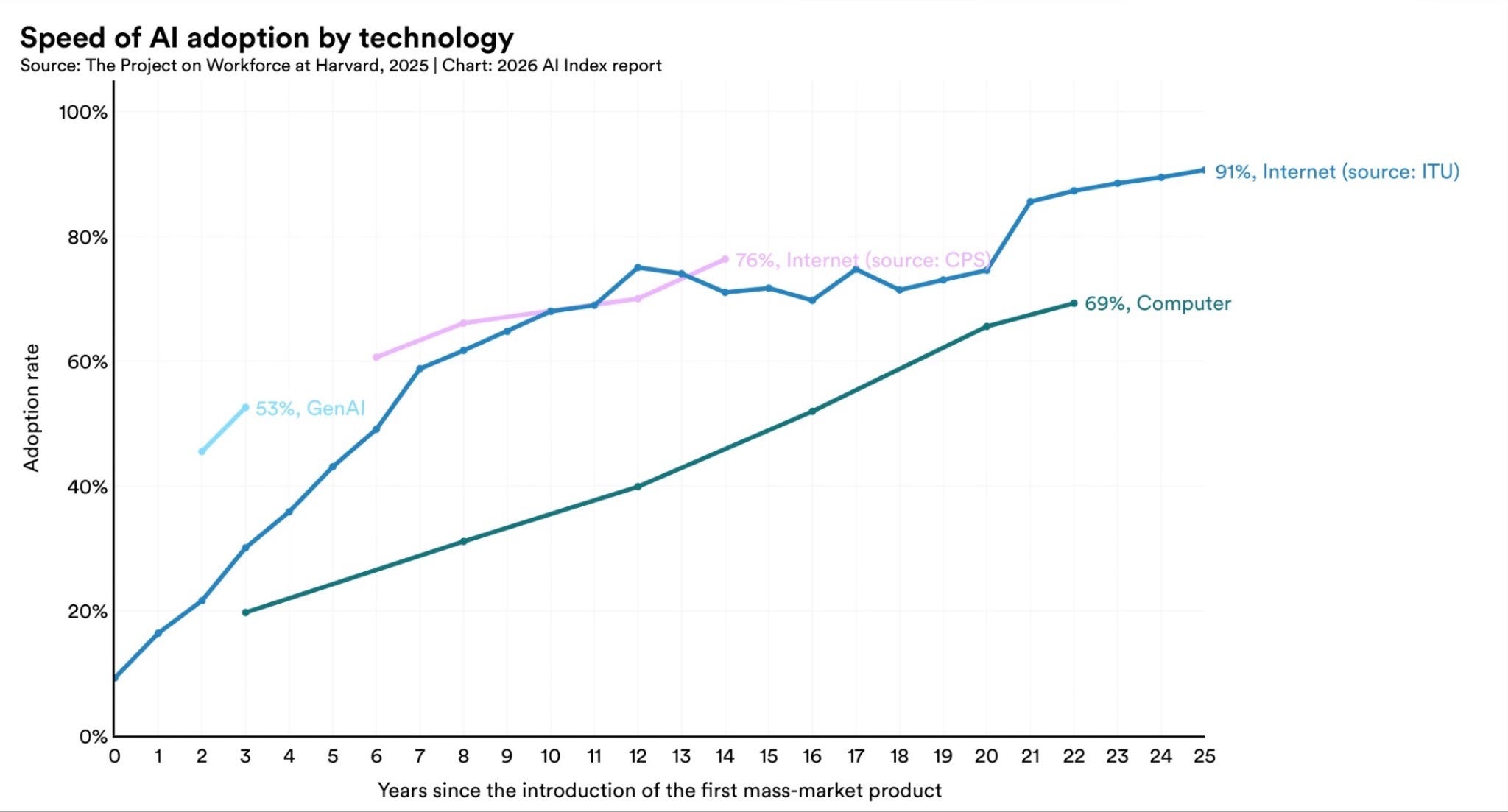

AI demand growth is unprecedented. Stanford’s 2026 AI Index Report found that Generative AI adoption reached 88% of organizations (up from 78% in 2025), and 53% of the population use AI. That rapid adoption within three years is faster than that of the PC or the internet.

AI capability continues rising fast. The same Stanford 2026 AI Index found that performance kept rising across model providers. On a key coding benchmark performance rose from 60% to near 100% in just one year. And compute capacity grew 3.3x per year since 2022.

Prices for chips and memory skyrocketed. TrendForce reported record highs for DRAM and NAND memory prices as suppliers prioritized higher-margin data-center demand. This increased cost pressure on consumer devices such as laptops and tablets. Apple already raised prices across the board in June 2026 since “The rapid expansion of AI data centers has created an extraordinary surge in demand for memory and storage.”

Closing Thought

SpaceX is the first AI behemoth to assemble this much leverage across the AI stack. It owns frontier-model infrastructure (xAI and Colossus), consumer distribution (X), and now also enterprise workflow (Cursor). It also sells infrastructure capacity to Anthropic and Google. Grok competes with Claude and Gemini, while SpaceX controls compute capacity both rivals depend on.

Infrastructure and hardware have become critical to AI. Data center capacity, GPUs, memory, power and cooling are becoming strategic constraints. Recent memory shortages have already flowed through to higher prices for consumer electronics. As AI demand and model capability keep rising, long-term access to infrastructure becomes critical for AI providers and the companies building on top of them.

For AI builders, the strategic risk is no longer limited to model access. In 2025, enterprises piloted AI use cases while large buyers consolidated individual layers of the stack. In 2026, those dependencies started consolidating together. When one supplier controls compute, identity, context and distribution, infrastructure costs, roadmap dependency, and pricing power become linked.

The companies that preserve leverage will know which control points they must own, which they can rent, and where they need a credible second supplier.